I originally was going to write an overview of the cost management process called Control Costs, but I decided to put it together with a review of the other two processes, Estimate Costs and Determine Budget, for reference.

1. Cost Management Processes Overview

Here’s a table giving a summary description of the three processes for an overview:

Figure 1. The Three Cost Management PM processes

| Process Group |

Process Number |

Process Name |

Process Description |

| Planning | 7.1 | Estimate Costs | Develops an approximation of the monetary resources needed to complete project activities.. |

| 7.2 | Determine Budget | Stage 1: Sums up the estimated costs to get the project estimate. Stage 2: Reserves are added to get the cost baseline and the cost budget. Stage 3: Periodic funding requirements are taken into account to get the final time-phased budget called the cost performance baseline. |

|

| Monitoring & Controlling | 7.3 | Control Costs | Carry out the cost management plan. |

Just a few words of clarification about the processes summarized in the paragraphs above.

7.1 Estimate Costs

There are two basic types of estimates: top-down (analogous and parametric) based on historical data of similar projects done in the past, and bottom-up methods (e.g., 3-point estimates) based on the WBS and risk analysis. Here are some points in distinguishing the various advantages and disadvantages top-down and bottom-up methods.

Figure 2. Comparison between Top-Down and Bottom-Up Estimates

| Top-Down | Bottom-Up | |

| Time | Quick | Time-consuming |

| Range of Accuracy of Estimates | Good for Rough Order of Magnitude (ROM) Estimates (-50%/+50% from actual costs) |

Good for Budget Estimates (-10/25%) If you add risk analysis, you can get Definitive Estimates (-5/+10%). |

| Project Type | Best for projects similar to those done before. | Best for research and development of new products. |

| Buy-In | Good for management buy-in of project charter | Good for buy-in of project team during planning |

7.2 Determine Budget

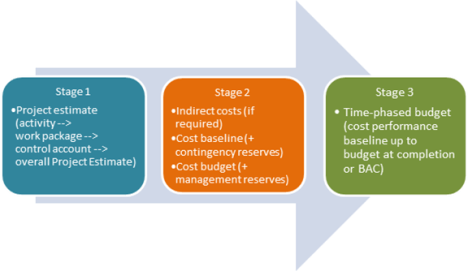

The three stages I mention above are not mentioned in the PMBOK® Guide; they are my own labeling invention to make sense of the process. It was found in our study group that splitting the process into three stages made sense because it not only clarified the steps of the process, but it allowed grouping of the inputs, tools & techniques, and outputs of the process into more logical subgroups.

Stage 1

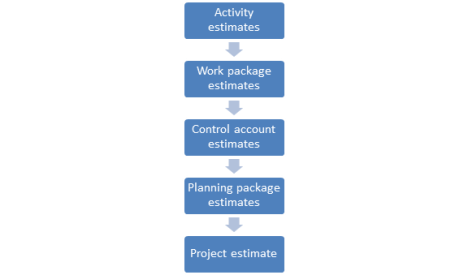

You add up all the activities to the level of the work packages, adding up all the work packages to the level of the control accounts, and then adding those up to get the final total: the project estimate, the sum of the direct costs of the project itself.

Note: There may be planning packages added if the project planning is using progressive elaboration. These are blocks of the WBS or work breakdown structure that don’t yet have a definitive estimate, usually in the later parts of the project. The project starts on the work that is detailed in the WBS for the first part of the project and which does have a definitive estimate. Then the planning packages are elaborated on and given those definitive estimates as the project gets closer to them. It’s like laying down the tracks for a train that is meanwhile coming down the tracks straight towards you.

Here’s a schematic for Stage 1 of the Estimate Costs process.

Figure 3. Stage 1 of the Estimate Costs Process

Stage 2

If there are project management costs that are not attributable to any one particular project, such as the costs of project management software tools (such as Microsoft Project), the company may decide to budget for these indirect costs by splitting them up in a specified way between the projects. If the company decides to do this, the indirect costs are added to the total direct costs, or project estimate, that was the end result of Stage 1.

Then two levels of reserves are added:

A. Contingency reserves

These are for risks accounted for in the risk register. They are added to the project estimate to get the cost baseline.

Project estimate + contingency reserves = cost baseline

Two things to note: a) contingency reserves can normally be used at the discretion of the project manager; b) the cost baseline is the basis for going on to Stage 3 of the process.

B. Management reserves

These are for unknown risks that are NOT accounted for in the risk register. They are added to the cost baseline to get the cost budget.

Cost baseline + management reserves = cost budget

Two things to note: a) management reserves, as the name implies, can normally only be used at the discretion of management, not the project manager; b) the cost budget is NOT the basis of carrying out the cost management plan, but rather the cost baseline is.

Below is a schematic that explains the process in Stage 2 of the Estimate Costs process.

Figure 4. Stage 2 of the Estimate Costs Process

Stage 3

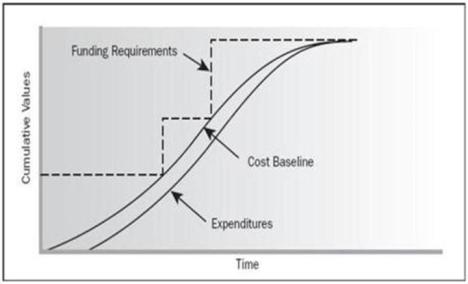

The cost baseline is the total costs of the project plus the contingency reserves. Then the costs for the project are spread out across the schedule of the project to get the cost performance baseline. See the diagram below taken from the PMBOK® Guide.

If this amount cannot be 100% funded by the company at the beginning of the project due to cash flow constraints, then it must be funded periodically during the course of the project. In this case, the project funding requirements have to be set up at various points along the project.

The Determine Budget process is summarized graphically below.

7.3 Control Costs

Essentially the Control Costs process consists of carrying out the Cost Management Plan. Where does this come from? The planning for cost management does not take place in any of the cost management processes listed above; instead the cost management plan is created as a component of the overall project management plan in the process 4.2 Develop Project Management Plan which is part of the Integration Knowledge Area. The various elements of the Cost Management Plan are listed on my post for 10/14/2012.

Here are the various steps of the control costs process as listed in the PMBOK ® Guide, but let’s use the methodology of Six Sigma called DMAIC or Define-Measure-Analyze-Improve-Control, to group them logically. Six Sigma is normally used for managing quality of manufacturing processes, but the methodology can be considered analogous to the process of managing costs on a project.

|

Stage |

DMAIC |

Control Costs Process element |

| Stage 1. | Define | The cost performance plan is where the cost management processes are defined and the criteria set forth for controlling project costs. |

| Stage 2 | Measure | Monitoring cost performance (CV, CPI) and work performance (SV, SPI) to detect variances from cost performance baseline. Monitoring cost expenditures (AC) so that they do not exceed periodic funding requirement limits. |

| Stage 3 | Analyze | Forecasting estimate at completion (EAC) and comparing to budget at completion (BAC) based on current trends. Using To-Complete Performance Index or (TCPI) to calculate level of cost performance that needs to be achieved to bring EAC in line with BAC by the end of the project. Determining the factors that create changes to the cost performance baseline. |

| Stage 4 | Improve | Corrective action to bring current cost overruns within acceptable limits. These actions can result in change requests, which are evaluated, approved/rejected, and implemented if approved.

Another type of change request is a change to the cost performance baseline if the current one is shown to be unrealistic. |

| Stage 5 | Control | Preventive action to bring future costs overruns within acceptable limits—these can also result in change requests (see above under Improve). |

In the next posts, I will go into the inputs, tools & techniques, and outputs of the Control Costs process using this five-stage description I have listed above.

Filed under: Uncategorized |

Leave a comment