The Theory of Constraints tries to make an operating system more efficient, i.e., more profitable, by analyzing its components into inputs, processes, and outputs, and then measuring them. Then constraints are removed to improve the system. This post talks about Throughput Accounting, which is a way of measuring the efficiency of a system. After this explanation, there will be a brief explanation of how this kind of accounting differs from the traditional type of accounting (particularly with regards to how it treats inventory).

1. What are the three basic measures of an operating system?

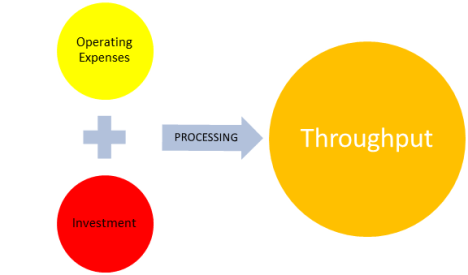

The way you measure the efficiency of an operating system is through what is called Throughput Accounting. The theory of constraints says that you try to maximize your output or throughput and minimize your input, of which there are two types, money or operating expenses and capital or investment.

Sales are an example of throughput; inventory, equipment, and real estate are the investments needed to run an operation, and the money it takes to actually create throughput would be the operating expenses.

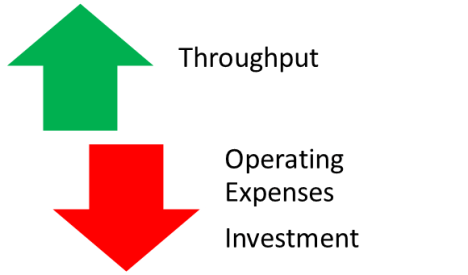

In general, the goal of an organization will be first to increase throughput, and next to decrease both operating expenses and investment.

2. What are the four derived measures of an operating system?

Given the basic statement in paragraph 1, that the goal is to first increase throughput and next decrease operating expenses and investment, let’s turn to the four derived measures of an operating system which are derived from the three basic measures.

| Derived Measure | Formula | |

| 1. | Net Profit | Throughput – Operating Expenses

|

| 2. | Productivity | Throughput / Operating Expenses

|

| 3. | Return on Investment (ROI)

|

Net Profit / Investment

|

| 4. | Investment Turns | Throughput / Investment |

1. Net Profit

The net profit can be increased by either increasing the throughput or decreasing the operating expenses.

2. Productivity

The same type of measure as “net profit”, but this time expressed as a ratio rather than the difference between throughput and operating expenses.

3. Return on Investment

This can be increased by an increase in net profit or a decrease in investment required to create that amount of profit. The net profit, in turn can be increased according to the two factors described above in paragraph 1.

4. Investment Turns

How much throughput is created per unit of investment? This is what is measured here.

3. Throughput vs. Traditional Accounting

The above measures are part of what is called Throughput Accounting. How does it differ from traditional accounting? The difference is most notable with inventory, which is part of investment. Traditional investment considers unused inventory as an asset, because it could theoretically be sold and become part of the throughput and thus contribute to the net profit. In reality, however, it just sits there and that is why inventory in Throughput Accounting is considered a liability, and not an asset. As a liability, the emphasis is on reducing it as much as possible.

Now that we have covered the way the Theory of Constraints measures the efficiency of an operating system, let us discuss in the next post the five focusing steps on how to increase the efficiency.

Filed under: Uncategorized |

Leave a comment